Social Equity Through Clean Energy

Who will you meet?

Cities are innovating, companies are pivoting, and start-ups are growing. Like you, every urban practitioner has a remarkable story of insight and challenge from the past year.

Meet these peers and discuss the future of cities in the new Meeting of the Minds Executive Cohort Program. Replace boring virtual summits with facilitated, online, small-group discussions where you can make real connections with extraordinary, like-minded people.

Across the country, the economic benefits of residential solar power have for the most part been available only to those who own their own homes and can afford the upfront costs of rooftop solar. 38% of households in the City of Baltimore qualify as low-income, 60% of whom are renters and thus by definition have been unable to benefit from residential rooftop solar.

At the same time, the average energy burden of low-income households in Maryland (the percentage of monthly income spent on energy) is six times that of non low-income households. So those who are in greatest need of electricity bill savings in Maryland have had the least access to them.

This emerging pattern of inequitable access to solar must be addressed as we transition to a clean energy economy. It needs to be addressed both because it is the right thing to do, and because low-income households make up 14% of the electricity market in Maryland and generate substantial greenhouse gas emissions. If fully served by solar energy, the low-income residential electricity market would reduce CO2 emissions by about four million metric tons, roughly 10% of the state of Maryland’s goal for 2030 GHG emission reductions.

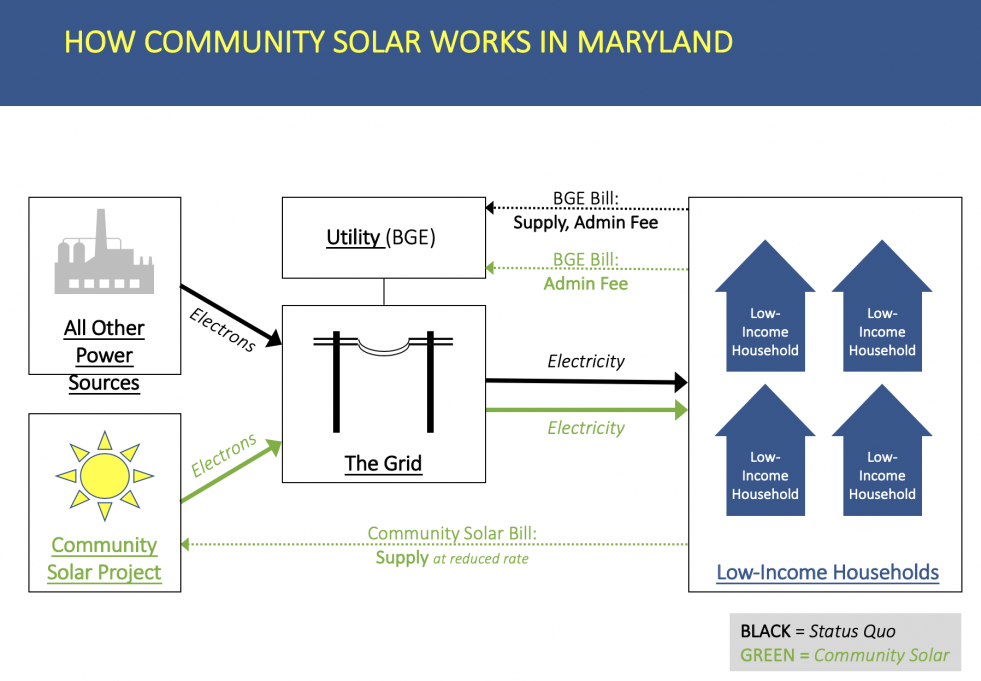

Community Solar in Maryland

In 2015, the Maryland General Assembly took action to remove this key barrier to low-income solar access. The General Assembly passed a law allowing households remote access to solar power: any Maryland resident, whether they own their own home or not, can sign up for solar power that is generated elsewhere in the same utility service territory and get credit on their electricity bill for that power. The Maryland Public Service Commission subsequently issued the Maryland Community Solar Pilot Program regulation in 2016.

The Climate Access Fund

The Maryland Community Solar Pilot Program requires that at least 30% of the program’s solar capacity be reserved for projects that serve low- and moderate- income (LMI) customers. Yet the regulation does not include any financial incentives for solar developers to serve LMI subscribers, and traditional developers and their investors tend to be hesitant to enter the low-income community solar market because they are concerned that low-income customers may not pay their bills.

The Baltimore-based Climate Access Fund (CAF), a nonprofit Green Bank, was launched in 2017 to address this gap between the community solar regulation and the way the solar market has traditionally worked. CAF provides a one-stop shop for low-income community solar, working to attract solar developers to the nascent market. CAF offers solar developers:

- Potential solar sites, with a focus on urban rooftops

- Attractive financing in exchange for savings to low-income participants

- Access to low-income subscribers through community-based partnerships

The attractive financing CAF offers is two-fold:

- Below-market debt with flexible terms (using loan capital raised through philanthropic program-related investments)

- A guarantee to cover potential revenue losses in the event of low-income subscriber non-payment (provided by the State of Maryland)

In exchange for these services, solar developers must agree to an initial 20% discount on low-income subscribers’ electricity bills, with no credit limitations or lengthy contract requirements.

CAF expects to close on its first project in the coming months, and has a pipeline of additional potential projects in the queue. CAF’s short-term goal is to maximize the number of low-income subscribers who can benefit from its community solar projects over the next four years (the remaining term of the Community Solar Pilot Program), thereby strengthening the case that the Program should be made permanent. CAF’s longer-term goal is to collect low-income bill payment data in order to demonstrate to the private market that traditional credit scores are not necessarily the best metric for electricity bill payment. CAF anticipates that its projects, owned by solar developers and their tax equity partners, will be refinanceable at market rates at the end of CAF’s seven year loan terms. CAF can then use its flexible capital to help kick-start another emerging clean energy market for low-income benefit.

By demonstrating that affordable community solar power can be successfully financed and deployed in underserved communities, CAF aims to help bring the market to scale in Baltimore and throughout Maryland.

Green Banks

CAF was created in partnership with the Coalition for Green Capital (CGC), and builds on the Green Bank model that CGC has developed and implemented. “Green Bank” is an umbrella term for financial institutions that seek to reduce greenhouse gas emissions while also reducing consumer energy costs. Green Banks achieve this by investing a dedicated pool of capital in ways that mobilize additional private investment.

In CAF’s case, we created a plan to establish a non-profit green bank that, instead of relying solely on public funds, would raise mission-driven dollars from multiple sources. By establishing a new Green Bank without direct government assistance, CAF takes a new and innovative approach towards the Green Bank model.

The proven track record established by US Green Banks is growing. Fourteen Green Bank institutions exist across the country, although they use varying names to describe their activities. Together they have mobilized almost $3.7 billion in investment into projects including clean energy and energy efficiency.

Additional state and local Green Banks are in development, and conversations at the national scale have taken note of existing Green Banks’ successes. One bill recently introduced in the Senate would funnel billions of dollars into state and local Green Banks as a way of mobilizing unprecedented public and private clean energy investment.

CAF is a key player in this broader movement, developing frameworks to bring affordable and accessible clean energy to the widest possible audience.

Discussion

Leave your comment below, or reply to others.

Please note that this comment section is for thoughtful, on-topic discussions. Admin approval is required for all comments. Your comment may be edited if it contains grammatical errors. Low effort, self-promotional, or impolite comments will be deleted.

Read more from MeetingoftheMinds.org

Spotlighting innovations in urban sustainability and connected technology

Middle-Mile Networks: The Middleman of Internet Connectivity

The development of public, open-access middle mile infrastructure can expand internet networks closer to unserved and underserved communities while offering equal opportunity for ISPs to link cost effectively to last mile infrastructure. This strategy would connect more Americans to high-speed internet while also driving down prices by increasing competition among local ISPs.

In addition to potentially helping narrow the digital divide, middle mile infrastructure would also provide backup options for networks if one connection pathway fails, and it would help support regional economic development by connecting businesses.

Wildfire Risk Reduction: Connecting the Dots

One of the most visceral manifestations of the combined problems of urbanization and climate change are the enormous wildfires that engulf areas of the American West. Fire behavior itself is now changing. Over 120 years of well-intentioned fire suppression have created huge reserves of fuel which, when combined with warmer temperatures and drought-dried landscapes, create unstoppable fires that spread with extreme speed, jump fire-breaks, level entire towns, take lives and destroy hundreds of thousands of acres, even in landscapes that are conditioned to employ fire as part of their reproductive cycle.

ARISE-US recently held a very successful symposium, “Wildfire Risk Reduction – Connecting the Dots” for wildfire stakeholders – insurers, US Forest Service, engineers, fire awareness NGOs and others – to discuss the issues and their possible solutions. This article sets out some of the major points to emerge.

Innovating Our Way Out of Crisis

Whether deep freezes in Texas, wildfires in California, hurricanes along the Gulf Coast, or any other calamity, our innovations today will build the reliable, resilient, equitable, and prosperous grid tomorrow. Innovation, in short, combines the dream of what’s possible with the pragmatism of what’s practical. That’s the big-idea, hard-reality approach that helped transform Texas into the world’s energy powerhouse — from oil and gas to zero-emissions wind, sun, and, soon, geothermal.

It’s time to make the production and consumption of energy faster, smarter, cleaner, more resilient, and more efficient. Business leaders, political leaders, the energy sector, and savvy citizens have the power to put investment and practices in place that support a robust energy innovation ecosystem. So, saddle up.

0 Comments