Building Integrated Vegetation

Who will you meet?

Cities are innovating, companies are pivoting, and start-ups are growing. Like you, every urban practitioner has a remarkable story of insight and challenge from the past year.

Meet these peers and discuss the future of cities in the new Meeting of the Minds Executive Cohort Program. Replace boring virtual summits with facilitated, online, small-group discussions where you can make real connections with extraordinary, like-minded people.

Mitigating Urban Environmental Challenges with Building Material Technologies

The rapid urbanization around the globe during the last five decades has come at a heavy price to the environment with rising air pollution, urban heat-island effect, and loss of biodiversity and green spaces. With increasing awareness about these issues, government bodies are looking at building-integrated vegetation (BIV) – green roofs and green walls – as a tool to mitigate the environmental degradation and improve livability.

BIV is Driven by City-Level Incentives and Mandates

Unlike other “green” sectors such as solar photovoltaic or biofuels, BIV adoption is not driven by national-level policy measures, but entirely by city-level hyperlocal priorities. Specifically, the two major types of policy drivers for BIV are:

-

Building code requirements and mandates.

Building code requirements on storm-water discharge such as those in London, mandates for green roofs such as those in Copenhagen, and mandates for green walls in Shanghai will drive adoption.

-

Financial incentives.

Financial incentives such as cash rebates for installing green roofs in Portland and exemptions in storm-water surcharge in London will shorten the payback period and the upfront capital expenditure.

Value Proposition against Competing Technologies is a Major Barrier for Adoption

Green roofs and walls offer a multitude of benefits such as reducing solar heat gain during summer, removing pollutants from ambient air, reducing storm-water volume, and increasing acoustic insulation. However, for every such benefit, a competing technology exists with arguably a better cost-to-performance tradeoff. Installed cost of $300/m2 to $500/m2 for green roofs and $900/m2 to $1100/m2 for green walls is an order of magnitude higher than technologies such as cool roof coatings that offer the thermal insulation benefits, photocatalytic coatings that remove pollutants from ambient air, and rainwater harvesting tanks that reduce the storm-water volume. Therefore, cities or building owners evaluating technologies to address a single environmental issue will likely not adopt green roofs or walls. Only cities that are looking at all possible environmental benefits of green roofs and walls will design supportive policy instruments.

BIV will be a $7.7 Billion Market by 2017

In the likely scenario, green roofs will be a $7 billion market by 2017 with a $2 billion opportunity for suppliers of polymeric materials such as geosynthetic fabrics, and waterproof membranes, the rest going towards vegetation, installation, and operating businesses. In the likely scenario, green walls will be a $680 million market by 2017, with a $200 million opportunity for suppliers of materials such as self-supporting polyurethane foam growth media.

-

Commercial buildings in North America and Asia-Pacific will be the growth segment.

Maturing Swiss and German markets will slow down their growth, but early-stage markets in the Americas and Asia-Pacific will provide significant growth opportunities. Commercial buildings in particular will be a key growth segment, due to the tolerance for high capital expenditure.

-

Finding right system integrator partners will be the key to success for materials suppliers.

Payback periods for BIV run in decades, and building owners are rightly concerned about water leaks, maintaining the vegetation, and ensuring that the roof or wall underneath the vegetation is able to withstand the additional weight. This dynamic creates a preferential market opportunity for reputable systems integrators with expertise across these diverse domains, and materials suppliers should seek such partners as a channel to market.

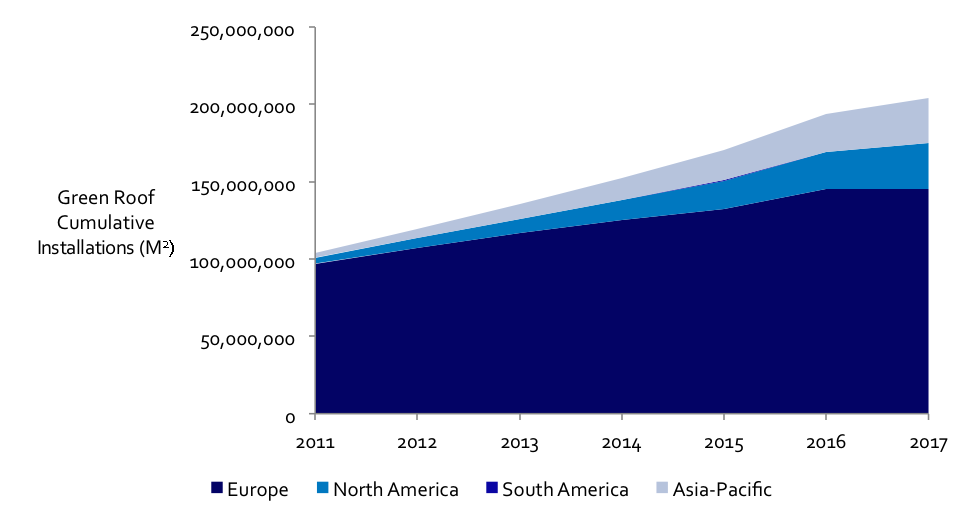

In the Most Likely Scenario, Cumulative Green Roof Installations Grow to 200 Million m2 by 2017

Figure 1 shows our five-year forecast of cumulative green roof installations, doubling from 120 million m2 in 2012 to 204 million m2 in 2017 at an 11.33% CAGR. Specifically,

-

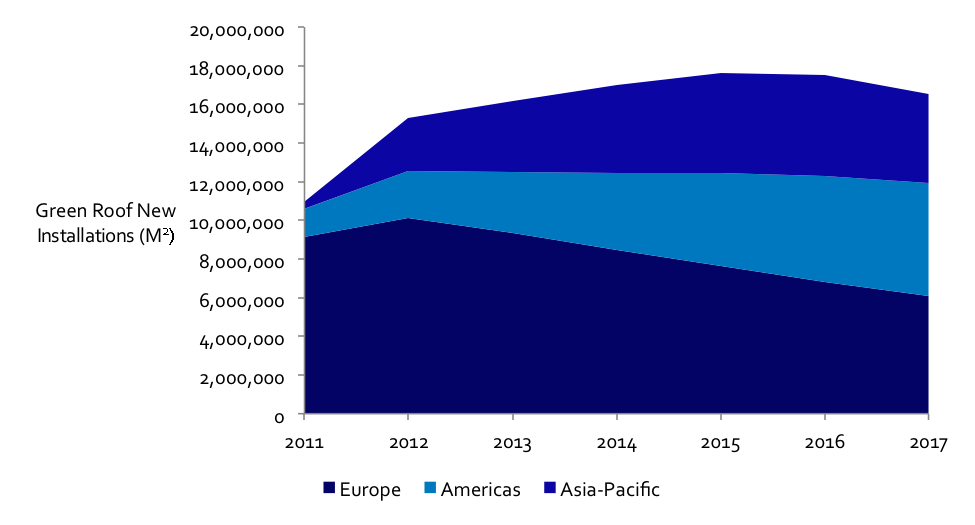

Green roof installations slow in Europe due to maturing markets in Germany and Switzerland.

Europe has led the growth of green roofs market in the last two decades. Germany alone commands a staggering 86 million m2 of installed green roofs, out of a cumulative 104 million m2 in 2011. However, markets in Germany and Switzerland are maturing and close to the saturation point. In Germany, 10% of all flat roofs are green roofs already. In Switzerland, the most prominent city with green roof mandates, Basel is already at 70% of its stated target for green roof installations. Therefore, as seen in Figure 2, Europe’s share of new capacity decreases from 83% in 2011 to 36% in 2017. Still, cities such as Copenhagen and London will provide growth opportunities even in this shrinking geographical segment.

Fig. 1: Cumulative Green Roof Installations Double over the Next Five Years

[margin20]

Fig. 2: Green Roof Market Size Split by Region 2011-2017: Most Likely Scenario

-

Coastal cities drive the growth in North America to an annual 5.8 million m2 in 2017.

The North American market is at an inflection point. A number of cities in the U.S. and Canada have announced mandates or incentives for green roofs. In addition, this market segment is far from maturity, with green roofs occupying less than a fraction of 1% of flat roofs. As a result, North America’s share of new installations increases from 13% to 35%. Expect to see cities like Portland, Toronto, and New York to lead the way, and cities with maturing green roof markets such as Chicago to drop in new installations.

-

Colombia and Peru sow the seeds for a burgeoning market in South America.

Use of recycled materials and frugal design principles has brought down the costs for green roofs in Colombia and Peru. In addition, the governments have announced supporting incentives in building code requirements and financing. As a result, there is already a budding market and credible local suppliers such as Biotectonica. However, given the size of these countries, the market at maturity is likely to be small. Therefore, we project that green roof new installations will grow modestly from 28,000 m2 in 2011 to 39,000 m2 in 2017. There are larger countries in South America, such as Brazil and Chile, which could potentially adopt green roofs. However, given the current level of negligible activity in those countries and the long purchasing cycle for green roofs, our likely scenario does not include any contribution from them.

-

Shanghai, Tokyo, and Sydney propel Asia-Pacific to an annual 4.6 million m2 by 2017.

The urgency to address urban environmental issues such as air pollution and storm-water management, cities such as Beijing, Shanghai, Tokyo, and Sydney have announced ambitious targets for green-roof installations. Starting at a small base, the Asia-Pacific market will not reach maturity until 2016 or even 2020 if additional cities such as Osaka decide to participate. We project that Asia’s share of new green-roof installations will rise dramatically from 3% in 2011 to 28% in 2017.

-

Optimistic scenario projects cumulative installations to an annual 28 million m2 by 2017, owing to a host of new cities adopting green roofs.

The participation of new cities such as Stockholm, Osaka, Kuala Lampur, and Mumbai propels green roof installations to an annual 28 million m2 by 2017 in the optimistic scenario. Lack of onboarding new cities and stagnant new construction on existing cities holds back growth across the board to an annual 12.5 million m2 in 2017.

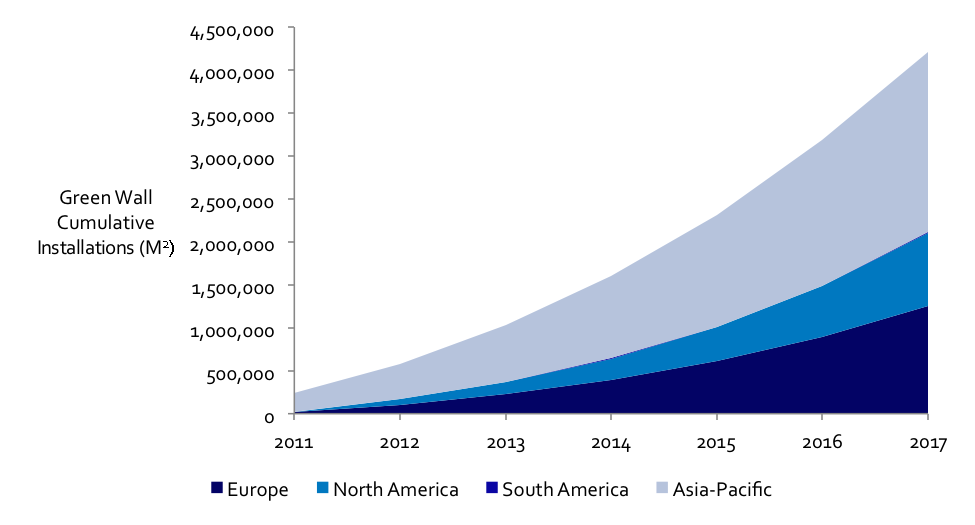

In the Most Likely Scenario, Cumulative Green Wall Installations Rise from 244,000 m2 in 2011 to 4.2 Million m2 by 2017

The green walls segment shows a dramatic increase in the forthcoming five-year period. Specifically,

-

Green walls is a nascent market and hence shows dramatic growth from 2011 to 2017.

Unlike the established green roofs market, green walls market is in its infancy. We project that in the likely scenario, vegetated walls get adopted at a fast clip, from 28,000 m2 in 2011 to 1.02 million m2 in 2017. The cumulative green wall installations rise from a small base of 244,000 m2 in 2011 to 4.2 million m2 in 2017 (see Figure 3). Building materials companies looking for an early-stage growth segment should identify system integration partners for joint development.

-

Asia-Pacific leads the pack.

The most prominent supporting policy measures for green walls exist in Asia, particularly China and Singapore. Hence, it is not surprising that the Asia-Pacific market share of green wall installations in 2017 stands at 40%. Europe and North America follow closely at 35% and 25% respectively, owing to adoption in showcase corporate and institutional buildings (see Figure 4). Colombia remains an early adopter of BIV technologies in South America with projects such as the eight-story green wall in Hotel Virrey, Bogota.

-

In all scenarios, all the regions are at an inflection point of growth for green walls.

Even in the low scenario, cumulative installations rise to 3.1 million m2 by 2017. In the high scenario, the cumulative installations rise to 6.1 million m2 by 2017. In the most likely scenario, the global market for green walls increases from $25 million in 2011 to $680 million in 2017.

Fig. 3: Cumulative Green Wall Installations Increase 16 Times over the Next Five Years

[margin20]

Fig. 4: Green Wall Market Size Split by Region 2011-2017: Most Likely Scenario

In trying to address ever-increasing urban environmental problems, cities around the world will adopt BIV technologies during this coming decade. However, significant challenges remain in performance measurements and estimating payback periods, and clients should expect to see the following trends emerge:

-

Financial concerns will dictate choice of vegetation.

To date, most green roofs and walls have incorporated sedum or other hardy plants that require little external irrigation. However, in the next five years, architects will choose specific vegetation to address food security or mitigate air pollution or retain storm-water. According to a leading architect and design firm in Southeast Asia, “vegetation selection will be a key performance differentiator as well as a design challenge for green roof and wall installations.” The increasing variety in vegetation beyond sedum to suit local conditions will present opportunities for a variety of customized porous materials.

-

Building materials companies will develop special grades of waterproof membranes and geosynthetic fabrics suited for BIV.

In the last two decades, building materials companies have used their standard roofing membrane, foam and fabric offerings, to market to the BIV segment. However, as the market becomes mainstream and performance standards more established, expect to see building materials engineered for higher compressive strength, water retention, and porosity than standard roofing applications.

-

Payback periods become an important metric.

In the last two decades, aesthetics, public relations, and corporate sustainability goals have driven BIV adoption. As a result, most technology developers today cannot give a good estimate of the payback period, which could go as high as 30 years. However, as the market grows beyond this niche, expect to see technology developers become much more sophisticated in their estimates of payback period to include city tax credits, cash rebates, storm-water tax savings, and energy savings. As BIV technologies compete for market share with mainstream energy efficiency technologies such as cool roof coatings, the technology developers will have to shorten the payback periods considerably.

-

BIV technologies increasingly integrate with other innovative building materials.

Green roofs reduce the operating temperature for photovoltaic panels located next to them, and improve their output. Green walls absorb the nitrate solid compounds from photocatalytic coatings neutralizing NOx and reduce the regulatory barriers for adoption. In future, expect to see synergistic combinations of BIV with BIPV, photocatalytic coatings, insulated glazings, and cool roofs. Companies developing these technologies – e.g. Sika Sarnafil, 3M, Dow, and AkzoNobel – will look to incorporate them in BIV solutions to capitalize on these synergies.

Discussion

Leave your comment below, or reply to others.

Please note that this comment section is for thoughtful, on-topic discussions. Admin approval is required for all comments. Your comment may be edited if it contains grammatical errors. Low effort, self-promotional, or impolite comments will be deleted.

3 Comments

Submit a Comment

Read more from MeetingoftheMinds.org

Spotlighting innovations in urban sustainability and connected technology

Middle-Mile Networks: The Middleman of Internet Connectivity

The development of public, open-access middle mile infrastructure can expand internet networks closer to unserved and underserved communities while offering equal opportunity for ISPs to link cost effectively to last mile infrastructure. This strategy would connect more Americans to high-speed internet while also driving down prices by increasing competition among local ISPs.

In addition to potentially helping narrow the digital divide, middle mile infrastructure would also provide backup options for networks if one connection pathway fails, and it would help support regional economic development by connecting businesses.

Wildfire Risk Reduction: Connecting the Dots

One of the most visceral manifestations of the combined problems of urbanization and climate change are the enormous wildfires that engulf areas of the American West. Fire behavior itself is now changing. Over 120 years of well-intentioned fire suppression have created huge reserves of fuel which, when combined with warmer temperatures and drought-dried landscapes, create unstoppable fires that spread with extreme speed, jump fire-breaks, level entire towns, take lives and destroy hundreds of thousands of acres, even in landscapes that are conditioned to employ fire as part of their reproductive cycle.

ARISE-US recently held a very successful symposium, “Wildfire Risk Reduction – Connecting the Dots” for wildfire stakeholders – insurers, US Forest Service, engineers, fire awareness NGOs and others – to discuss the issues and their possible solutions. This article sets out some of the major points to emerge.

Innovating Our Way Out of Crisis

Whether deep freezes in Texas, wildfires in California, hurricanes along the Gulf Coast, or any other calamity, our innovations today will build the reliable, resilient, equitable, and prosperous grid tomorrow. Innovation, in short, combines the dream of what’s possible with the pragmatism of what’s practical. That’s the big-idea, hard-reality approach that helped transform Texas into the world’s energy powerhouse — from oil and gas to zero-emissions wind, sun, and, soon, geothermal.

It’s time to make the production and consumption of energy faster, smarter, cleaner, more resilient, and more efficient. Business leaders, political leaders, the energy sector, and savvy citizens have the power to put investment and practices in place that support a robust energy innovation ecosystem. So, saddle up.

Aditya,

Thank you for this insightful look into the future for the green roof industry. I’ve been researching roof statistics for this kind of information and have had a difficult time of it. I’d love some advice on where to look for current percentage of flat roof space and current uptake.

Aditya,

Thank you for this informative research. It is a very good market forecast for those of us trying to understand where the living wall market is heading.

Dear Aditya,

thank you very much for the interesting data. Do you by chance have data regarding indoor green walls?